Lead in Cyber Insurance:

Boost Sales, Reduce Risk

Sell, underwrite, and manage cyber insurance with less risk and greater confidence, efficiency, and profitability – all powered by our patented cyber insurance AI orchestration technology – Vivaldi™

TRUSTED BY INDUSTRY LEADERS

Understanding cyber insurance risk is complicated. We make it easy.

Designed for cyber insurance

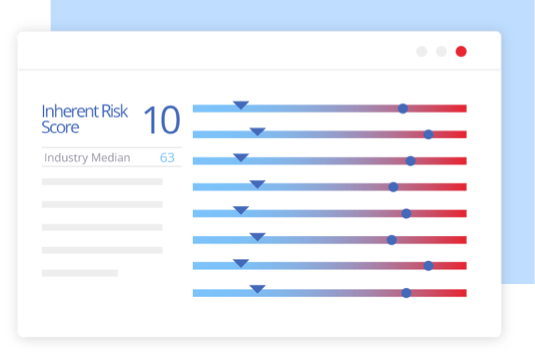

Unparalleled Accuracy

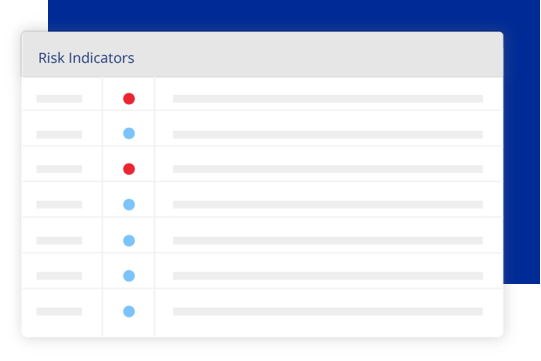

Deep Insight

Broad Scope

Tailored to Coverage

Global Reach

REAL-WORLD IMPACT

100m+

Data in less than a minute on 100M+ businesses

<25%

Record-Low Loss Ratios Achieved by Cyberwrite Customers

One platform to accelerate value across the cyber insurance lifecycle

For insurers

Increase Underwriting Profitability

Reduce underwriting costs and achieve record-low loss ratios with faster, more consistent underwriting decisions.

Improve Portfolio Management

Gain greater visibility into your organization’s aggregated risk exposure and ongoing monitoring of each company’s risk.

Boost Distribution Efficiency

Better target sales efforts with cyber risk insights on any business, at any time.

Empower Insureds

Provide insureds with actionable insights to reduce their cyber risks and mitigate losses when cyberattacks do occur.

For reinsurers + Lloyd’s Syndicates

Improve Portfolio Management

Get the cyber insurance risk data you need for every company across your portfolio to improve catastrophe modeling and risk management.

Ensure Global Consistency

Provide easy-to-understand cyber risk reports to your cedent companies to ensure consistency in underwriting.

Empower Insureds

Provide insureds with actionable insights to reduce their cyber risks and mitigate losses when cyberattacks do occur.

For agents and brokers

Grow Your Business

Become a trusted cyber risk advisor with personalized cyber insurance risk reports on any business in seconds to help your clients understand their cyber risks

Accelerate Sales

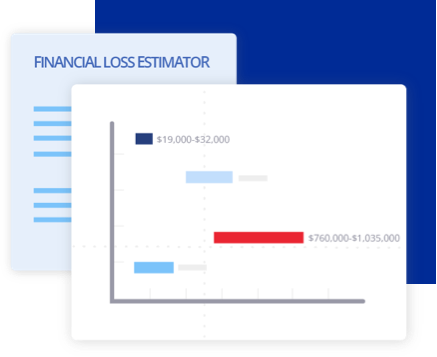

Drive adoption with ability to provide clients in real-time a clear understanding of the potential financial impact of a cyberattack on their business.

Empower Your Clients

Provide insureds with actionable insights to reduce their cyber risks and mitigate losses when cyberattacks do occur.

Reduce E&O Risks

Easily highlight the minimum coverage recommended to show clients why they need cyber insurance coverage.

What our customers say

Cyberwrite’s technology helps our customers reduce the risk of cyberattacks and protect their essential data, The strength and reach of Cyberwrite’s platform helps us keep up with emerging exposures in this rapidly evolving cyber threat landscape.

Tim Zeilman VP and Global Product Owner for Cyber HSB

With Cyberwrite, we are taking a leap forward in the evaluation, monitoring, and control of cyber risk, obtaining insights that are very useful for the teams to make data-driven underwriting decisions.

Oscar Taboada Head of Underwriting Europe & Head of Cyber MAPFRE RE

Creating a Cyberwrite report is easy and takes only a few minutes. The agent or broker inserts a company’s name, web address, sector, and location into the system… to calculate the applicable risk level, how much coverage is needed and of what type.

Tyler O’Connor Broker CRC Group

Cyberwrite gives our clients an insight into cyber risk, including critical findings and a potential loss estimate that clearly illustrates how much their exposure is. Having access to Cyberwrite has given our brokers a tremendous advantage and our clients confidence in their decision to purchase cyber insurance, and how much to purchase.

Edward Wong

Regional Director Howden Broking

Using the Cyberwrite risk reports enabled me as a broker to help clients get the policy they need. It’s easy to generate the report, but the level of risk analysis and potential financial impact predictions are really top-notch. Using the report we are able to explain cyber risk to customers quickly and easily.

Tony Cabot CEO Victor Insurance